The first Registered Investment Advisor dedicated to crypto

| What We Do

A Cutting Edge Approach to Asset Management

At DAIM we focus on crypto wealth management to help you achieve your financial goals without being deterred by market volatility and complexity.

Full Service Asset Management Company

Talk to Real Humans

When Clients Call DAIM they are answered by experienced advisors who can answer any of their digital asset investment questions.

Wondering How To Buy Bitcoin?

We handle the entire process from funding to asset management. You get regular reporting and 24/7 access.

Licensed & Secure

We are a licensed RIA (CRD# 294098) and partner with regulated trusts and full reserve custodians.

IRAs

We can put Bitcoin and other digital assets into all types of IRAs: Roth, Traditional, SEP, SIMPLE, and Solo 401k. However you're saving for retirement, we got you covered!

Save On Taxes

Our experienced team is familiar with strategies from tax loss harvesting to backdoor Roth Conversions.

Managed Account

Most crypto platforms leave you to invest alone, not us. As a fiduciary we offer a managed strategy to all clients.

ACHIEVEMENTS

#1 Ranking

In US 172% Growth in year-over-year Assets Under Management*

#2 Ranking

IN US 256% Growth in year-over-year number of clients*

Nominated

For the Orange County Business Journal 2022 Innovator of the Year award.

*2022 Registered Investment Advisor (RIA) Rankings Published in Financial Advisor

Total Return

0%

Trailing 12 Months

0%

Past performance is not a guarantee of future results. Read more here

OUR PLEDGE

Trust

As a fiduciary, our clients always come first. We provide transparent and personalized services, guided by a commitment to ethical and responsible practices. We conduct rigorous due diligence to ensure we partner with properly qualified entities. Our license can be found here on the SEC’s website

Security

Assets are held at a licensed custodian and held 1:1, not commingle or factored out. Multiple forms of authentication are required to transfer assets. We use conventional banking partners like JP Morgan and State Street.

We help clients buy Bitcoin and cryptocurrencies directly in their brokerage and tax-advantaged retirement accounts like 401ks and IRAs. Our long standing Model Portfolio is great for investors looking for professional management.

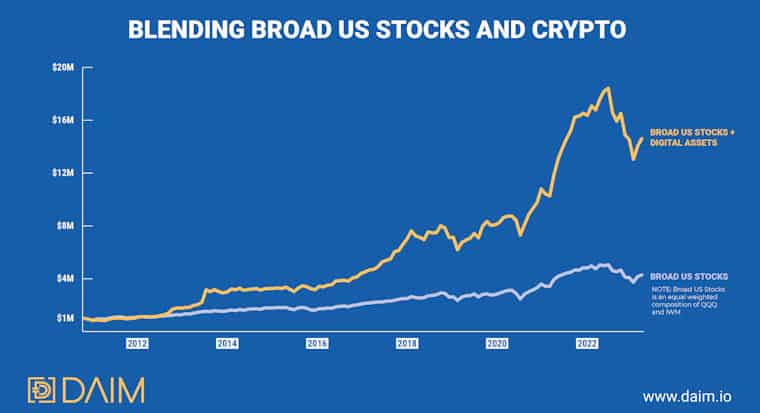

DAIM’s Equity & Crypto Portfolio is for qualified individuals seeking to combine a traditionally managed equity portfolio with pure cryptocurrencies. Clients may also choose to start solely with mutual funds and slowly add in crypto when desired.

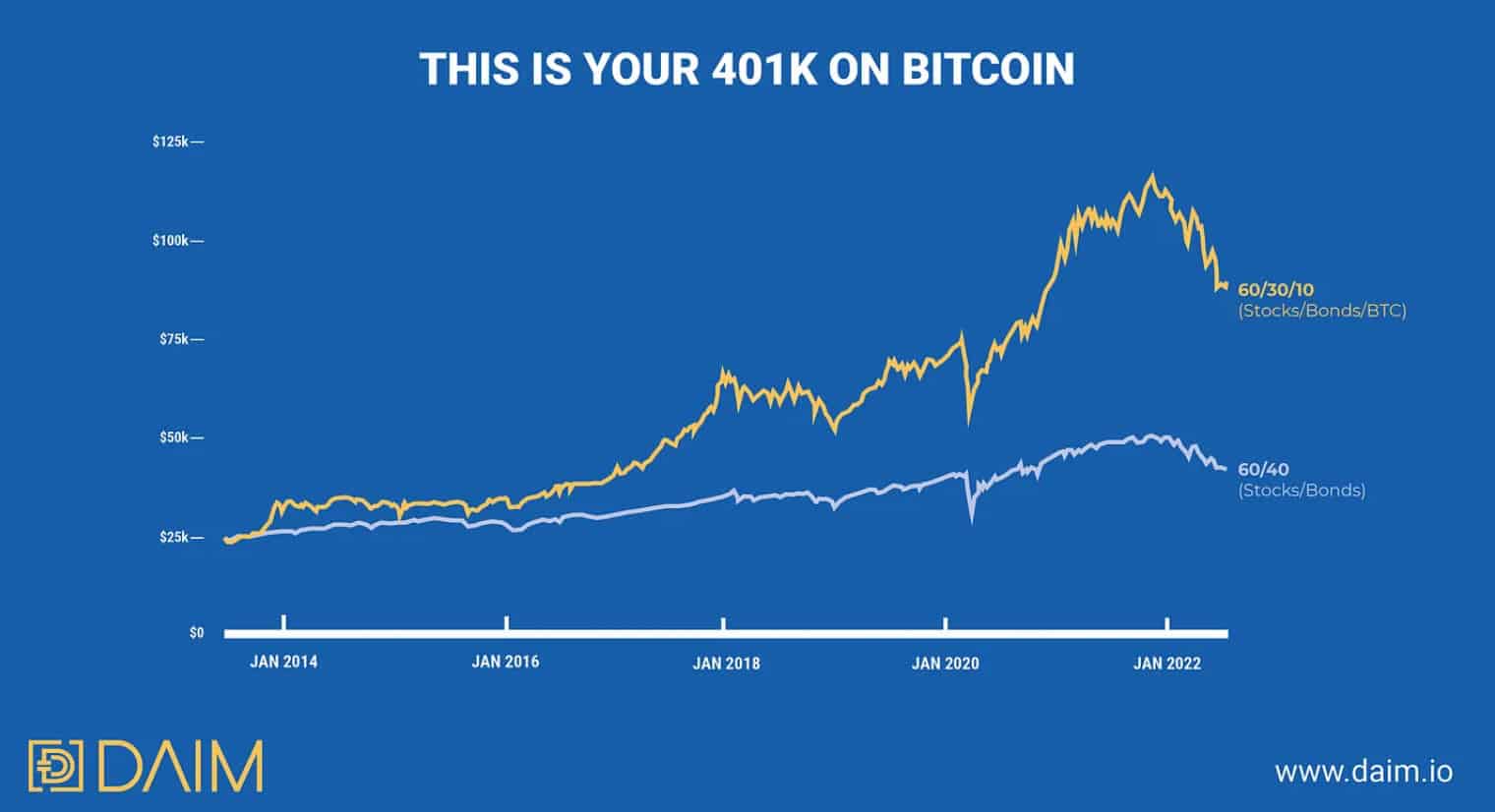

Employers now have the ability to offer 401k plans with the option of direct exposure to Bitcoin to complement a select stack of Vanguard mutual funds.

A Cutting Edge Approach to Asset Management. At DAIM we focus on crypto wealth management to help you achieve your financial goals without being deterred by market volatility and complexity.